Investor Selectivity Reshaping Venture Capital

India’s venture capital landscape is undergoing a fundamental transformation. The era of aggressive expansion and growth-at-any-cost is giving way to a more disciplined, selective investment environment. While capital remains available, investors are now applying significantly higher standards, prioritising profitability, unit economics, and governance over mere growth narratives .

💰 Funding Recovers, But Discipline Tightens

Venture capital funding in India has steadily recovered from the sharp slowdown of 2023, reaching approximately $16 billion in 2025 . However, the nature of capital flowing into startups has changed fundamentally.

Key data points from H1 2026:

- Indian startups raised $7.39 billion across 701 rounds, up 9.4% year-on-year

- However, the number of funding rounds plummeted 41%, from 1,189 to 701

- Seed and early-stage funding: $3.34 billion across 608 rounds, up from $2.96 billion across 1,055 rounds a year earlier

- Average cheque size nearly doubled to $5.5 million from $2.8 million

The divergence between funding value and deal activity is stark. Investors are deploying larger amounts of capital into a smaller pool of companies while remaining cautious on early-stage investments . As Anand Lunia, founding partner at India Quotient, noted: “Funds of our size or bigger ones are doing more or less the same amount of activity. But angel syndicates are fewer and smaller firms are tighter” .

🎯 What Investors Are Looking For

Profitability as the New Filter

The diligence bar has reset. Investors are no longer rewarding growth without visibility on profits, governance, and long-term sustainability . Accel India Founding Partner Prashanth Prakash observed: “There is a significant shift towards companies that are able to demonstrate the ability to get to ₹50 crore–₹100 crore of EBITDA within 7-8 years of operation” .

Key metrics investors now evaluate:

- LTV:CAC ratio of 3:1 is the gold standard

- CAC payback period under 18 months

- Clear path to profitability

- Strong governance frameworks

The trend is visible across sectors. Companies with stronger EBITDA margins relied less on fresh capital issuance and had a higher share of offer-for-sale components in their IPOs . In effect, stronger businesses are increasingly using IPOs as liquidity events rather than survival funding exercises .

Selectivity Across Stages

Investors noted that even when evaluating consumer companies, one of the first things they look at is whether the founder is “AI-enabled or AI-first” . The cost structure of startups is changing—“earlier it was about people; today it is about people and tokens” .

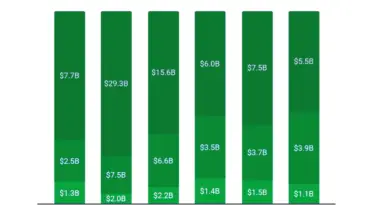

📊 Sectoral Shift: Where Capital Is Flowing

Investors are gravitating toward resilient, domestically anchored sectors :

- Deep Tech & AI Infrastructure – AI funding surged 317% YoY to $676 million in H1 2026

- Manufacturing & Industrials – Investments rose ~55% year-on-year

- Consumer & Retail – Rose 2.6 times year-on-year

- Semiconductors, SpaceTech, Advanced Materials – Emerging as priority sectors

The shift reflects a broader transformation: investors are moving away from heavily cash-burning internet models and toward businesses that deliver measurable efficiency and long-term value .

🤝 Exit Evolution: Beyond IPOs

While IPOs have increasingly become a mainstream exit route, investors are widening their playbook .

IPO Landscape

- 21 PE/VC-backed companies raised about ₹52,514 crore through mainboard IPOs in 2025

- 53 startups went public in 2025, raising ₹29,200 crore

- However, recent technology IPOs have faced delays amid market volatility

Secondary Transactions and M&A

Secondary activity has become more institutionalised :

- 51 secondary VC transactions worth $1.1 billion in 2025

- 214 startup M&A deals worth $6.7 billion in 2025

- Founder buybacks, strategic sales increasingly seen as valid liquidity routes

Nao Murakami, founder and general partner of Incubate Fund Asia, noted: “We think there is an opportunity for about $50 million to $60 million in secondary transactions in this financial year” .

💡 What This Means for Founders

The message from investors is unequivocal: build with sharper focus on unit economics, governance, and long-term resilience .

Actionable priorities for founders:

- Profitability is no longer optional – Over one-third of Indian startups chose profitability and runway extension over fundraising in 2025

- Demonstrate capital efficiency – Investors are rewarding disciplined CAC/LTV ratios

- Build defensible moats – Focus on products anchored in novel technology and engineering that are difficult to replicate

- Prepare for longer preparation cycles – Seed rounds now require more mature products and clearer commercial paths

- Consider hybrid approach – The best startups are achieving both profitability and growth through disciplined execution

🔮 Outlook

India’s venture capital ecosystem enters 2026 with strong structural fundamentals but heightened selectivity. Domestic capital now accounts for nearly 50–55% of active investors, compared with 35–40% for global peers . Family offices, mutual funds, and retail investors are playing a larger role .

Siddarth Pai, founding partner at 3one4 Capital, noted: “The minimum viable products coming to market now are a lot more mature, courtesy of AI. Even non-technical people can use AI to create a prototype, get some traction and then raise funds” .

The next phase of growth will be defined less by capital availability and more by investors’ ability to deploy capital with discipline . Patience, governance, and earnings—not hype—will decide outcomes .