India Emerges as Asia’s Leading FinTech Investment Destination

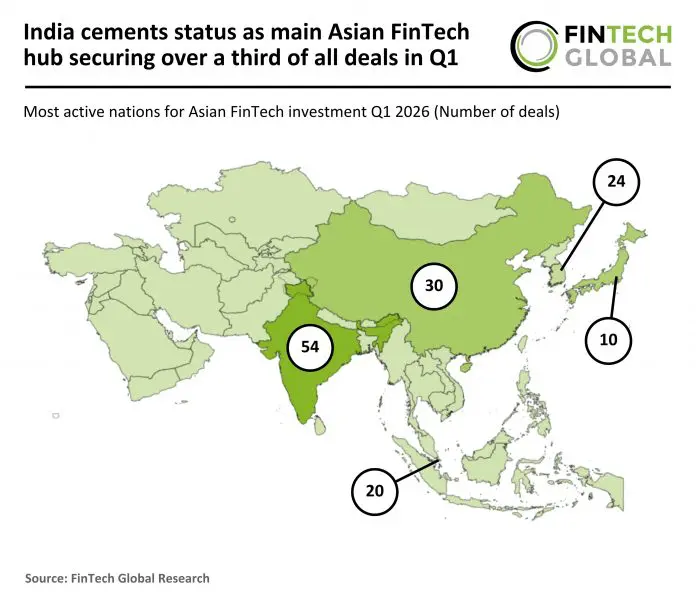

India has solidified its position as the most active fintech market in Asia, securing more than one-third of all fintech deals in the region during the first quarter of 2026 . With 54 deals and a 35% share of total activity, India maintained its dominance, up from 46 deals and a 28% share in Q1 2025—a 17% rise in volume that also translated into a notable gain in its proportional standing .

📊 Q1 2026 FinTech Funding at a Glance

| Metric | Value |

|---|---|

| Total FinTech Deals in Asia | 153 deals ($1.8bn) |

| India’s Share of Deals | 54 deals (35% share) |

| India’s Funding (Q1) | $844.5 million (59% YoY increase) |

| Average Deal Size | $18.4 million (24% YoY increase) |

| Late-Stage Funding | $273 million (126% QoQ increase) |

📈 A Maturing Market: Fewer Deals, Larger Cheques

India’s fintech ecosystem raised **$513 million across 45 funding rounds** in Q1 2026, compared to $503 million through 99 rounds in Q1 2025 . While total funding increased marginally (2% YoY), the sharp decline in deal count—from 99 to 45 rounds—signals a clear shift toward selective, quality-focused investing .

“Q1 2026’s defining feature is the gap between funding and deal count. Aggregate funding was nearly flat against Q1 2025—but round count fell from 99 to 45. The same capital is now concentrated across less than half the companies, pointing to a material rise in average cheque size and a far more selective investor stance.”

— Tracxn Geo Quarterly Report

This trend reflects a maturing ecosystem where investors are prioritising scale, profitability, and execution over rapid, unchecked expansion .

🏙️ Mumbai Emerges as the New FinTech Capital

Mumbai overtook Bengaluru as India’s leading fintech funding hub, capturing 61% of total investments ($311 million) in Q1 2026, up from just 9% in Q1 2025 . This shift tracks the rise of lending and affordable-housing fintech—sectors where Mumbai’s proximity to banks, NBFCs, and insurance capital is a structural advantage .

Bengaluru followed with 30% ($152 million), while Gurugram, Delhi, and Chennai together contributed less than 10% . Four of the five largest deals in Q1 2026—Weaver ($156M), Ecofy ($15M), Easy Home Finance ($30M), and IDfy—were from Mumbai-based companies .

💼 Key Drivers of India’s FinTech Leadership

1. Digital Payments Maturity

India’s digital payments infrastructure has entered a phase of deep structural maturity. Digital payments now account for a dominant share of retail payment volumes, with UPI serving as the default rail for digital transactions . The ecosystem is now witnessing verticalisation of UPI—savings-led, rewards-led, and credit-led use cases are emerging as distinct categories .

2. Expanding Financial Inclusion

Fintech platforms are increasingly targeting underserved populations, bringing millions into the formal economy . From Bharat-first lending platforms to vernacular wealth management apps, the focus has shifted to unlocking the next 100 million users through:

3. AI-Driven Infrastructure Innovation

Artificial intelligence is fundamentally reshaping BFSI operations—from collections and back-office processing to fraud detection and sales enablement . Credit-infrastructure firm Knight FinTech, which raised $23.6 million in Accel-led Series A, exemplifies this trend, building AI-native platforms for co-lending, risk intelligence, and automated underwriting .

4. Lending and Wealth Management Growth

Online lending accounted for 60% of total fintech funding in Q1 2026 . KreditBee achieved unicorn status in April 2026, joining Juspay (valued at $1.2 billion) as recent additions to India’s fintech unicorn cohort .

🔮 The Road Ahead: IPO Pipeline and Regulatory Unlocks

India’s fintech ecosystem is poised for significant developments in 2026:

Upcoming Fintech IPOs

Companies expected to file DRHPs or go public include PhonePe, Razorpay, PayU, KreditBee, Moneyview, Kissht, Fibe, and Turtlemint—representing ~$30 billion in potential value to be unlocked in the public markets .

Regulatory Tailwinds

- GIFT City is moving beyond a regulatory sandbox to become a real fintech hub, enabling easier cross-border finance, global investing, and NRI banking

- DPDP Act implementation in 2026 will overhaul data practices, creating compliance opportunities for tech-enabled platforms

- Co-lending and Credit on UPI are creating new distribution channels for fintech-bank partnerships

🎯 Investor Sentiment: Selective But Confident

Investors are placing greater emphasis on revenue visibility, capital efficiency, and scalable distribution models, rather than prioritising rapid customer acquisition alone . Regulatory compliance has emerged as a central consideration in funding decisions—companies securing licensing approvals or aligning closely with oversight frameworks are better positioned to attract institutional capital .

Key investment themes for 2026 include:

| Theme | Opportunity |

|---|---|

| Agentic Payments | New rails for AI-to-AI transactions |

| AI Wealth Management | Digital-first, GenZ-focused advisory |

| Fraud Prevention | Deepfake KYC and anomaly detection |

| Bharat Lending | Aspirational lending for travel, gadgets, lifestyle |

| Fintech Infrastructure | Co-lending, Credit on UPI, BBPS |

✨ The Final Word

India’s emergence as Asia’s leading fintech investment destination is not coincidental. The country’s digital public infrastructure, financial inclusion momentum, and AI-driven innovation have created a conducive environment for fintech growth. While the funding landscape has become more selective, with capital concentrating in fewer, more mature companies, the long-term trajectory remains robust.

As one industry observer noted, “The signal is not retreat, but selection: investors are writing bigger cheques into fewer, later-stage companies with demonstrated unit economics” .

With a strong IPO pipeline, regulatory tailwinds from GIFT City and the DPDP Act, and continued innovation in AI-powered financial infrastructure, India is well-positioned to maintain its leadership in Asia’s fintech landscape throughout 2026 and beyond.